11990 Grant St., Suite 550 Northglenn, CO 80233

How to Use Your Amortization Schedule

Net Admin • November 7, 2017

There are fewer things as rewarding as finally closing on your home loan. We know there are a lot of hoops to jump through, and a lot of paperwork you must provide to us in order to make this happen. In return, what happens at closing? More paperwork! Of course, it’s all very important paperwork regarding your home and loan so it’s necessary but one of the often overlooked pieces of that stack of closing papers is the Amortization Schedule.

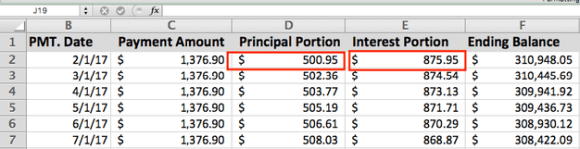

The Amortization Schedule is about seven pages long but details exactly how much of your mortgage payment is applied toward principal, interest and PMI if that’s part of your home loan program.

It’s sometimes overlooked that each mortgage payment, while consistent if you have a fixed rate mortgage, is actually the sum of separate values each month. In the example below, there is no PMI (private mortgage insurance) included in this mortgage type so the payment amount is the sum of the principal and the interest.

What you’ll notice is the Principal Portion increases each month while the Interest Portion diminishes each month, shifting the balance of where your monthly payment is applied. Great, so what does this matter to you?

Eliminating Payments Without Paying the Full Payment Amount

You can eliminate payments by paying an additional Principal Portion with your monthly payment. For example, if you were on payment #5, and you wanted to pay additional principal, you would look to the “Principal Portion” on payment line #6, and pay that amount.

Payment Amount: $1,376.90

Additional Principal: $506.61

Total Payment: $1,883.51

By paying the Principal Portion of payment #6, you have eliminated the Interest Portion of payment #6. This does not mean that you don’t make your next regularly scheduled mortgage payment. It simply means that the next payment you make will be payment #7, rather than payment #6.

It is easier to pay additional principal in the earlier years of the loan because this is when the Principal Portion will be the lowest. This makes it a bit more feasible for making additional principal payments should you receive a bonus, or have some extra cash lying around.

The Amortization Schedule and eliminating payments can be confusing. I would be happy to talk with you, and explain it in a bit more detail should you have any questions.

We always appreciate feedback here, so feel free to reach out.

Brett is a native to Colorado, being born and raised in the Denver Metro Area. Growing up, he learned the value of financial responsibility and gravitated toward an industry that allows him to counsel and coach clients about financial goals as it relates to Real Estate. Brett joined the lending industry in 2003. Throughout his career he has helped many families achieve their goals and dreams of home ownership. From First Time Home Buyers to Real Estate Investors, Brett has the knowledge and experience to tailor loans to your unique and specific situation. Working with Brett and Prosper Mortgage Group, LLC, you can rest assured your loan is in great hands with professionals that deal with this daily. Customer service, honesty, and integrity have set him apart from his competition while keeping his focus on the Clients’ best interest, determining the best possible loan for each individual situation, & helping them achieve their goals and dreams of homeownership! Through these principals, Brett has built a very successful career basing much of his business on the referrals of past clients as well as the Real Estate Professionals that he works with. Brett relies on personal responsibility, accountability, and mental toughness in his daily life and is a huge advocate of the 75 Hard / Live Hard program as well as personal development. NMLS 253202 CO MLO 100015587 Prosper Mortgage Group, LLC NMLS 2490880 Equal Housing Lender Inside Westminster is proudly sponsored by: Prosper Mortgage Group—helping you Own Your Future. NMLS #2490880 | Equal Housing Lender I 303.668.5891 I www.prospermortgagegroup.com Westminster Chamber 303.961.5975 www.westminsterchamber.biz

In today’s tech-savvy world, social media is a key aspect of how many people stay connected and find entertainment. But social media is also great for other things, including the homebuying process. Follow these tips to find your new home while you’re scrolling through your feed.Start by adding real estate agents to your feed, as …

The home market is booming. If you are a first-time homebuyer or someone who has not owned a home for a three-year period, you may qualify for a no down payment program. Typically, these programs are available through your local county, state, or government. Here are four types of no down payment programs that can …

Restrictions have been placed upon movement and travel, as well as everyday events such as shopping and education being impacted. As we move towards the fall, the threat presented by the situation has not subsided sufficiently enough for life to return to normal, with several US States seeing a spike in cases. That means, as a …

Thinking of turning your home into a long-term rental? There are several different reasons why homeowners make this decision. If your home has been on the market for a while and you’re having trouble getting offers at your asking price, renting it out may be a better option than taking a loss on your sale. …

Change is the new normal these days. How about for the housing market and mortgage rates? Will rates move another leg lower or is this the bottom? What’s next for them? There are 3 things to track as we move through summer: Spikes in coronavirus cases in several states: This is a real concern that comes …

The process of buying a new home can, at times, be frustrating and intimidating. While each step is important, several factors must be considered, or you may end up with a home that doesn’t suit your needs. Of all the factors to think about when buying a home, location is critical. When it comes to

What is the first thing someone sees when they drive up to a house for sale? In most cases, it’s what the house looks like from their vehicle. It’s known as curb appeal, the look and feel of a house when looking at it from the street or the curb. And it can tell a homebuyer a lot about a …

There is nothing like the thrill of moving into a new home. Whether you’re moving into your first home or your fifth, however, there are some important things you will want to ensure make it onto your todo list. Let’s take a look. Change Your Locks. This is one safety measure you want to take right …

We have a brief update in these days of constantly changing information in response to the uncertainty of the coronavirus and its impact on our country. The Fed has cut the Fed Funds Rate by 1.50% in the last couple of weeks, including 1.00% on Sunday, March 15th alone. Messages in the media are confusing …